Sustainability Terms

A Sustainability Glossary: Definitions for Executives, Strategic Planners, Practitioners

Sustainability is increasingly being integrated into high-level decision-making at corporations, public sector agencies, non-governmental organizations, and other groups. This brings many benefits but can also create challenges, including vocabulary issues. To help bring more clarity, we’ve compiled these definitions of sustainability terms.

When economic, environmental, and social metrics are considered together, it’s important for sustainability practitioners to understand the terms and concepts of traditional financially oriented analysis, and for executives to have a grasp of the metrics and frameworks that now allow environmental and social considerations to be incorporated into project evaluations.

We hope this sustainability glossary will prove useful to both groups, and serve as an aid to effective collaboration. These sustainability definitions were prepared by EarthShift Global LLC in collaboration with our colleague John Parker, chief product officer and co-founder of Impact Infrastructure, developers of Autocase, with input from the EarthShift Global team. We thank John for his excellent efforts, and invite our readers to send suggestions for other terms or words they’d like to see added.

The glossary includes terminology related to supply-chain assessments that consider environmental, social and/or economic dimensions -- for example, terms related to life cycle assessment (LCA) and triple bottom line assessments. Terms are shown in alphabetical order.

A

Accuracy: How close a measurement is to the actual value. See also Precision

Acidification (oceans): Acidification refers to the change in oceanic pH due to the absorption of atmospheric carbon dioxide. Oceans are a natural carbon buffer because they take up about one-fourth of all atmospheric carbon dioxide.

However, as atmospheric CO2 concentrations continue to increase, additional CO2 dissolves in water and increases the hydrogen ion concentration, thus making the water more acidic – about 30% more acidic due to human activities. The accompanying figure from NOAA shows the correlation between rising levels of carbon dioxide in the atmosphere at Mauna Loa with rising CO2 levels in the nearby ocean at station Aloha.

As more CO2 accumulates in the ocean, the pH of the ocean decreases. The acidification of oceans affects the ability of calcifying organisms to build their shells and skeletons needed for survival. Corals, crabs, sea stars, sea urchins, and plankton are some of the organisms affected. These organisms are essential to maintaining marine life, as they are at the bottom of the food chain.

Allocation: The process of attributing corresponding shares of environmental impact to a product in cases of multifunctionality/coproduction. For instance, in the case of recycling, there are two functions: waste management and creation of scrap material. In this case it is necessary to allocate the impacts to each of these functions. Some of the most-used principles in allocation are partitioning, system expansion, avoided burden, 50/50, and the cut-off method. While there is constant debate in the literature with regards to the most suitable method, in the end the issue of allocation is an artifact of the Life Cycle Assessment framework and as such there is no single best solution. For this reason, is important that practitioners test multiple approaches and assess whether and how the outcome of the study is affected.

Avoided burden: A type of EOL method. In the avoided burden method, the system boundaries are expanded such that the first life is credited for the recycling of the product by subtracting the avoided environmental burdens of the extraction of an equivalent amount of virgin materials. The first life is assigned all of the life-cycle burdens from extraction through to waste handling, as well as the environmental burdens of the recycling/refurbishment process. However, the first life is also credited with avoiding the environmental burdens associated with the extraction of virgin materials. In the second life (i.e. the use of the recycled material), the system is assigned the full life cycle burdens from raw material extraction through to EOL, including the virgin burdens avoided by the first life.

B

Benefit Cost Ratio (B/C Ratio): The present value of benefits divided by present value of costs. The Benefit Cost Ratio is used in go / no-go, whether-to-proceed decisions. It indicates dollars of benefit per dollar of cost, with a ratio greater than one indicating that the project is worthwhile. Caution is advisable when using this method, as the definition of benefits and costs and negative values can affect interpretation. Further information is available on Wikipedia.

C

Carbon footprint: Analysis focusing on the life-cycle climate-change impacts of a product or service. Therefore, results are typically presented as a single indicator in equivalent kilograms of carbon dioxide (kg CO2 eq). Guidance is included in the ISO 14067 standard.

Climate change: Climate change is a general term for impacts caused by the emission of carbon dioxide (CO2) and other heat-trapping gases, such as methane (CH4) and sulfur hexafluoride (SF6). These greenhouse gases (GHGs) absorb infrared light from the sun. Emissions are assessed by their radiative forcing, which is a measure of their ability to absorb infrared light. Naturally occurring GHGs keep the earth warm enough to support life. Man-made emissions increase infrared absorption, resulting in an increase in the average global temperature and causing various localized climate changes. Flora and fauna adapt to climate change at different rates, affecting species diversity. Human health is affected by increases in malaria and other tropical infectious diseases, heat stress, and flooding among others.

Cost Benefit Analysis (CBA): also known as Benefit Cost Analysis (BCA), is a formal way of organizing the evidence on the good and bad effects of projects and policies. The objective of a CBA may be to decide whether to proceed with a project, to see if the benefits justify the costs, to place a value on a project, or to decide which of various possible alternatives would be most beneficial. To facilitate comparison of different projects, or alternatives of the same project that may have costs and benefits occurring in different years, discounting is often used to convert future benefits and costs to a current-year perspective. The best criterion for deciding whether a project can be justified is whether the Net Present Value (NPV) is positive. The NPV is the discounted monetized value of expected net benefits (i.e., benefits minus costs). Other metrics (such as the return on investment, internal rate of return, benefit cost ratio, simple payback period, or discounted payback period) can also be used to summarize the CBA results. CBA is the primary methodology underpinning sustainable return on investment (S-ROI), and triple-bottom-line CBA (TBL-CBA). Further information on Wikipedia.

Cumulative Energy Demand (CED): An impact category that sums different categories of energy. Measured in MJ.

Cut-off method: The cut-off method is the simplest method used to model end-of-life (EOL). When a product is recycled at EOL, the cut-off method draws the boundary such that the product (first life) does not get any environmental credit for recycling, but also takes no environmental burden for waste handling. In the case of a product being made from recycled material (i.e the second life), the cut-off method assigns the burden of recycling/refurbishment entirely to the product (second life). No portion of virgin material is assigned to the product in this case.

D

Discounted Payback Period: is the number of years or months until capital is recouped by flow of benefits or cash flow. The Payback Period is used to determine timing of the project or the length of time during which capital is at risk. A shorter payback means less risk. The Discounted Payback Period uses discounted benefits or cash flows. In other words, the cash flows from the project are discounted by the discount rate before determining the payback period. For this reason, the Discounted Payback Period is usually longer than the Simple Payback Period. Further information on Wikipedia

E

Economic Impact Analysis (EIA): calculates the economic impact of a project in terms of net jobs created, Gross Domestic Product (GDP), and/or income created. Impacts can be direct (from project expenditures), indirect (from project suppliers’ expenditures), and induced (from the spending of wages of those affected); they can be estimated from input-output tables of the economy. Impacts such as GDP, jobs, and taxes, which all scale with the project dollars spent, are a poor measure of value. As long as you spend money you will generate income, output, jobs and tax revenue - the more you spend the bigger the impacts. While these statistics may have public relations value, there are more reliable and impartial statistics for measuring welfare or value. A simple example is that if a company hires skilled workers to build a project by hiring them away from other jobs (a likely scenario) then there are no net jobs created. It is now well-known that GDP is a measurement of economic activity that includes both helpful and harmful activities and is therefore not a suitable metric for sustainability (or ecological economic) analyses. Growth of the economy can be economic growth (producing net benefit) or uneconomic growth (depleting natural capital and producing net detriment). Further information on Wikipedia

Ecosystem Quality (endpoint): The number of species that may disappear due to a given impact, times the area over which they are affected, times the duration that the species are affected. Assessed in units of species * yr.

Egalitarian: one of three types of weighting perspective that can be used during analyses; it’s a long-term assessment, 500-year Global Warming Potential, that conservatively considers impacts that are not yet widely accepted. See also Hierarchist and Individualist.

End of Life (EOL): refers to the life cycle stage describing the last portion of a product’s useful life. This can either be disposal, reuse or recycling.

Environmental Product Declaration (EPD): see Type III Ecolabel.

Eutrophication: Eutrophication is when an excess of nutrients (nitrogen and phosphorus) causes an abnormal growth of algae in waterways. As algae die and oxidizes, it depletes the oxygen in the water (a phenomenon known as hypoxia). Excess nutrient runoff to waterways comes from fertilizers and sewage. Algae need four main ingredients to grow: light, carbon, nitrogen and phosphorus. They can only grow as much as the least available nutrient will allow. Therefore, when excess nitrogen-rich fertilizer runoff enters the ocean (which is normally nitrogen limited), algae grow. Similarly, freshwater is phosphorus limited, so the intrusion of sewage (high in phosphorus) can cause algae blooms.

F

50/50 (fifty-fifty): The 50/50 is an end-of-life (EOL) method developed to avoid the potentially complex modeling and data required to model real-world conditions for recycling (see Market-Based approach). In this approach, the system boundary is drawn between the first and second life of the product, with 50 percent of environmental burdens assigned to the first life, and 50 percent to the second. This approach is somewhat arbitrary and is designed to simply avoid having to deal with the complexity of other approaches. See also Cut-Off Method.

Functional unit: The functional unit is the basis for a product life cycle study and reflects the service provided by that product. Be as specific as possible. For example, in the case of laundry detergents, a functional unit can be the amount of detergent needed for a standard medium load. If the purpose of the detergent is to treat particularly soiled clothes, then it is necessary to factor in how much of the product is needed to provide clean clothes. Food products can be evaluated by weight or (if being compared with different options) by nutritional content such as calories, protein, and vitamins. Identifying the functional unit of some products/services may be challenging, as in the case of cloud storage or a smartphone. Overall, make sure the functional unit reflects the purpose of the product. If you are not sure, you can evaluate the results over different functional units. Choosing a proper functional unit is of particularly high importance in comparative LCAs.

G

Goal and Scope Definition: This is the first stage of an LCA, where practitioners establish a clear purpose for the study (goal) and define how much the LCA will cover (scope). An LCA can have two main objectives: comparison of several alternatives in order to select one (comparative assessment), or the identification of opportunities for improvement (improvement assessment). In a comparative assessment, multiple products are evaluated simultaneously to identify the product with the least environmental impact, while an improvement assessment typically covers a single product or service. The goal in the latter case is to find “hotspots” where the majority of impacts are coming from, so they can be reduced. When an LCA performs an analysis from raw material extraction all the way to final disposal it is called a cradle-to-grave analysis. Alternatively, cradle-to-gate LCAs can exclude use phase and disposal.

Greenblushing: Dix & Eaton define greenblushing as “limited or no information disseminated by an organization so as to understate or ignore its commitment to, and actions on, environmental and social responsibility.” Organizations who engage in greenblushing are taking valid environmental or social actions but do not communicate them.

Greenhouse gas (GHG): Greenhouse gases are gases which absorb infrared light. GHGs include carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O) among others. Naturally occurring GHGs keep the earth warm enough to support life. Man-made emissions increase infrared absorption, resulting in an increase in the average global temperature and causing various localized climate changes.

Greenwashing: Greenwashing is the process of conveying a false impression or providing misleading information about how a company's products are more environmentally sound. Greenwashing is considered an unsubstantiated claim to deceive consumers into believing that a company's products are environmentally friendly. For example, companies involved in greenwashing behavior might make claims that their products are from recycled materials or have energy-saving benefits. Although some of the environmental claims might be partly true, companies engaged in greenwashing typically exaggerate their claims or the benefits in an attempt to mislead consumers. The U.S. Federal Trade Commission (FTC) offers several illustrations of greenwashing on its website, which details its voluntary guidelines for deceptive green marketing claims. (Source: Will Kenton)

H

Hierarchist: one of three types of weighting perspective that can be used during analyses; it relies on consensus scientific perspectives. One example would be a medium-term assessment, 100-year Global Warming Potential, that assumes as a default the current temporal and technological policies. (See also Egalitarian, Individualist)

Human Health (endpoint): Accounts for the number of person-years lived as disabled as well as lives cut short. Measured in Disability-Adjusted Life Year (DALY).

Human toxicity: An impact category that represents a variety of substances that are detrimental to human health. The effects range from low impacts, like a cough, to severe ones like cancer and acute poisoning. To express all of these impacts in one measure, some methods compare the damages to a reference substance like 2,4-D (2,4-Dichlorophenoxyacetic acid, the component in Agent Orange), or combine them with respect to the extent of their disability in the unit DALYs (Disability Adjusted Life Years). DALYs are composed of the number of years living with a disability plus years lost due to premature death.

I

Impact Assessment: In an LCA, impact assessment comes after inventory analysis and links emissions of a product or stage to potential environmental impacts. For example, what are the impacts of sulfur oxides (SOX) emissions on human health and global warming? What are the effects of methane compared to carbon dioxide? Which one affects global warming the most? Impact assessment converts the emissions and inputs into expressions of their potential environmental effect(s). To do this, LCA databases define impact categories that reflect the impacts to the ecosystem, resources, and human health. The most common impact categories are: Climate Change, Ozone Depletion, Eutrophication, Ecotoxicity, Acidification, and Human Health. For example, the Climate Change impact category is measured in tons of carbon dioxide (CO2) equivalents and represents the global warming potential of a substance. Other substances with heat trapping properties are also in this category, such as methane, a greenhouse gas that traps about 20 times more heat than CO2 on a per-mass basis. Therefore, 1 ton of methane equals 20 tons of CO2 equivalents. Other substances like nitrogen oxides (NOX) contribute to Acidification and Eutrophication. The factor that converts one substance to another based on an environmental impact is called a characterization factor. LCA databases have characterization factors for most substances depending on the medium they are released in (air, water, or soil).

Impact category: In order to assess and compare the potential harm caused by a product, we categorize the environmental impacts of its creation. Examples include global warming and ozone depletion. Simply put, an impact category groups the emissions of various substances into a quantified measure of effects on global or local environments. They provide a means of examining the potential net harm of a product.

Individualist: one of three types of weighting perspective that can be used during analyses; it involves short-term assessment (20-year Global Warming Potential), assumes technology will address future problems, and considers only obvious and agreed-upon impacts. See also Egalitarian and Hierarchist.

Internal Rate of Return (IRR): is a measure of profitability or investment efficiency. IRR is a discount rate that makes the net present value (NPV) of all cash flows from a particular project equal to zero. IRR may give better insights than return on investment (ROI) in capital-constrained situations. However, when comparing mutually exclusive projects, NPV is the appropriate measure. Further information on Wikipedia.

ISO Standards: The International Organization for Standardization (ISO) is an independent, non-governmental body that brings together representatives from 167 nations to develop and update consensus standards for a wide range of technology and manufacturing activities, from date and time formats to child car seats and quality management.

ISO currently lists over 15 standards and publications related to life cycle assessment. An additional 65 standards and publications related to different aspects of environmental management, ranging from environmental management systems and environmental labeling to greenhouse gas management and carbon footprints are also available. The breadth and importance of the ISO standards make it worthwhile to review what the standards are, why they’re important, and how they’re developed — including firsthand observations from EarthShift Global analysts who are active in such development efforts. Click here for a full list of the ISO standards related to LCA, as well as other ISO environmental standards.

Inventory Analysis: The Inventory Analysis phase of an LCA comes after the “Goal and Scope” definition phase. The inventory tracks the resources and emissions coming in and out of the system. For instance, corn requires fertilization during the growing process, so the inventory quantifies the emissions embedded in the production and use of fertilizer. If the corn is packaged, then the resources, energy and emissions linked to the production and disposal of the packaging are also attributed to corn. Likewise, the manufacturing of farming equipment as well as its energy consumption during use is also attributed to corn. The inventory can be understood as the “list of ingredients” in the supply chain of a product.

L

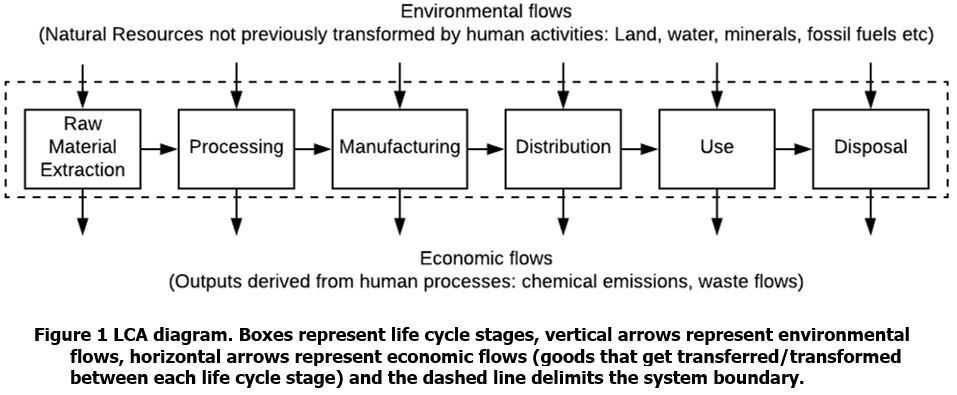

Life Cycle Assessment: a framework to quantify the systemic environmental impacts of a product or service. It consists of accounting for the environmental inflows and outflows of all processes in the supply chain of a product: from extraction of raw materials (cradle) to the final disposal or recycling (grave). The accompanying figure shows a representation of the life cycle of a product with its inputs and outputs.

Each stage converts energy and materials into a part of the product and, in the process, releases some emissions to the air, water, and/or soil. Because disposal is part of the life cycle of the product, the energy and resources required for actions like trash collection, transportation, and landfilling are also attributed to the product. One strength of LCA is its ability to look at multiple environmental impacts, not just climate change. Considering only consider greenhouse gas emissions results in a limited understanding of the entire system that created the product. Consideration of multiple impacts ensures that improvements in one aspect do not result in deterioration elsewhere, a phenomenon called burden shifting. For example, a product’s greenhouse gas emissions might be reduced by implementing a process that requires more water – this would not be detected in an analysis that considers only climate change.

Life Cycle Costing (LCC): or Life-Cycle Cost Analysis (LCCA), quantifies all financial costs of a project alternative. The financial costs in LCCA include up-front capital expenditures, ongoing operations and maintenance costs, replacement costs, and the residual value of assets at the end of the life cycle. LCCA is typically thought of from the perspective of a user of a product, process or investment. Alternatively, companies can use the concept to assess new product development efforts by considering research and development costs, piloting, launch, lifetime revenues, and the cost to retire the product when it becomes obsolete. The financial costs of each alternative are discounted into present value terms to account for different timing of costs. LCCA is not akin to LCA because it only quantifies financial costs, not environmental or social costs. LCCA has been used to encourage users to adopt more-sustainable products, such as LED or compact fluorescent lamps, where the up-front cost is higher, but the product lasts longer and costs less to operate than traditional alternatives. Further information on Wikipedia.

M

Midpoint result/Characterized result: a point of analysis in life cycle impact assessment that consists of results of midpoint impact categories.

Multiple Account Cost Benefit Analysis/Stakeholder Analysis: provides a breakdown of the costs and benefits to multiple parties, or accounts. These can include financial or direct financial value to a company, and pros and cons for governments, economies, and the environment, as well as Envision categories like quality of life, leadership, climate and risk, natural world, or resource allocation. Multiple Account Cost Benefit Analysis effectively does a mini-CBA [ADD ANCHOR LINK] for each stakeholder group (such as users or beneficiaries of a project, government or taxpayers, non-users living nearby, etc.) or account (such as the environment or local economy). This allows a project sponsor to understand each group’s perspective and think about how to structure a deal so that benefits and costs are equitably distributed. Sustainable Return on Investment and Triple Bottom Line Cost Benefit Analysis (TBL-CBA) are forms of multiple stakeholder/account cost benefit analysis, in which the accounts are financial, social, and environmental. Multiple account CBA makes CBA more relevant in helping to understand stakeholder objections and provides a framework for working towards a project that benefits all of society as well as sub-groups within that broader context.

N

Net Present Value (NPV): is the present-day value of benefits minus present-day value of costs. It is calculated by discounting cash flows over time and summing the discounted values. Cash flows further into the future are discounted more deeply. This metric allows the time-value of money to be taken into account. NPV is a measure of worth or value that can be used in go/no-go, whether-to-proceed decisions. An NPV greater than zero means project is economically efficient. Projects or alternatives can be ranked in terms of NPV, to provide a more-accurate reflection of value to the business. Further information on Wikipedia.

Normalization: The process of scaling characterized results to a common unit. Typically the characterized result of a study is compared to the performance of an external reference (such as regional or global per-capita annual impact) or an internal reference (another alternative within the options considered – minimum, maximum or average). The use of external references is most common in LCA. The normalization process involves dividing the characterized result of the study by the reference; this results in the units for all indicators being in a per year basis. Normalization has three purposes: 1) Checking for inconsistencies by evaluating the order of magnitude of results. Consumer products, for example, should be a fraction of the per-capita impacts (typically with a normalized result of a magnitude between 10^-9 and 10^-14). 2) Evaluating relevance in improvement assessment. Issues with the highest normalized scores are deemed more relevant and higher priorities for improvement efforts. However, there is a risk of bias in this procedure due to gaps in the normalization references, and also because of inverse proportionality issues (issues with the most pressing issues – large normalization value- are given a smaller normalized value systematically). 3) Preparation for weighting, which typically takes the form of a weighted sum. It is important to note, however, that normalized results should not be used to evaluate comparative results unless equal weighting is assumed.

O

Ozone depletion: Ozone layer depletion is simply the wearing out, or reduction, of the amount of ozone in the stratosphere. Unlike pollution, which has many types and causes, ozone depletion has been pinned down to one major human activity. Industries that manufacture products like insulating foams, solvents, soaps, and take-out food containers, and cooling equipment like air conditioners and refrigerators, use chemicals called chlorofluorocarbons (CFCs). These substances are heavier than air, but over time, (2-5 years) they are carried high into the stratosphere by wind. Depletion begins when CFC’s get into the stratosphere and ultraviolet radiation from the sun breaks them up. The breaking-up action releases chlorine atoms, which react with ozone, starting a chemical cycle that destroys the good ozone in that area. One chlorine atom can break apart more than 100,000 ozone molecules. There are other Ozone Depleting Substances (ODS) such as methyl bromide (used in pesticides), halons (used in fire extinguishers), and methyl chloroform (used in industrial solvent production).

P

Partitioning: For of allocation for multifunctional processes. Partitioning can be done on according to different relationships between co-products such as their relative: energy content, mass of production, or their respective economic value. The sum of the coefficients adds to 1.

Precision: How close repeated measurements are to the same value. See also Accuracy.

Product Category Rule (PCR): PCRs define how an LCA must be conducted for an Environmental Product Declaration and what must be reported. The PCRs typically mandate modeling choices such as allocation method and impact assessment method and may also identify acceptable or mandated data sources. PCRs are governed under ISO 14025 and in more detail in ISO 14927.

Program Operator: A program operator is responsible for managing the creation of Product Category Rules and certification/verification of Environmental Product Declarations. The role is defined by ISO 14025.

R

Radiative forcing: The ability of an emission to absorb infrared light.

Resources (endpoint): Puts a future monetary value on resources which will be made unavailable by using them today.

Return on investment (ROI): The benefit created by the investment of resources in a project. ROI can be expressed as: (profit, gain or benefit of investment minus cost of investment) divided by (cost of investment). As a performance metric, ROI is used to evaluate the efficiency of an investment or how efficiently the investment is used. ROI can be used to compare the efficiency of several different investments. Further information on Wikipedia.

S

Simple Payback Period: is the number of years or months until capital is recouped by flow of benefits or cash-flow. The Payback Period is used to determine timing of the project or the length of time capital is at risk. A shorter payback means less risk. The Simple Payback Period uses non-discounted benefits or cash-flows. In other words, the cash-flows from the project are taken at their nominal value to determine the time until the project pays back. For this reason, the Simple Payback Period is usually shorter than the Discounted Payback Period. Further information on Wikipedia.

Social Return on Investment (SROI): is a principles-based method for measuring extra-financial value (i.e., environmental and social value not currently reflected in conventional financial accounts) relative to resources invested. The SROI method accounts for stakeholders' views of impact and puts financial 'proxy' values on those impacts identified by stakeholders which do not typically have market values. While SROI is similar to S-ROI or CBA it is different in that it specifically excludes environmental impacts. In addition, some SROI users employ a version of the method that does not require that all impacts be assigned a financial proxy. Instead the "numerator" includes monetized, quantitative but not monetized, qualitative, and narrative types of information about value. While this type of information is typically included in SROI reports, the goal is to monetize as much as possible. Further information onWikipedia.

Sustainable Return on Investment (S-ROI): is an enhanced methodology for cost-benefit analysis (CBA) that includes probabilistic assessment and stakeholder engagement. The framework takes into account the entire scope of risk-adjusted costs and benefits related to sustainable design, including traditional internal cash impacts (such as savings on energy or water costs), but also all other appropriate internal and external non-cash impacts (such as the dollar value of environmental savings from reduced potable water use or air emissions). The analysis results in different sets of output metrics in terms of probabilities; one from the perspective of the organization on a cash flow basis and others from the perspective of various stakeholders, including society or future generations, which often includes the value of externalities such as health and safety benefits expressed in dollars. Finally, the analysis allows for transparency and incorporates a process for expert and stakeholder opinion on the model structure and inputs.

T

Terrestrial acidification: Soil acidification (the lowering of soil pH) occurs when inorganic substances such as sulfates, nitrates and phosphates are deposited on the soil. Life Cycle Assessment focuses on acidification from airborne and waterborne emissions, such as acid rain. Fertilization can also contribute to acidification. Acidification of the soil changes the plant types which thrive and can deplete nutrients available for plant uptake, affecting species diversity and crop production.

Triple Bottom Line Analysis (TBL): evaluates a project or policy based on its combined financial, social and environmental impacts (sometimes known as profit, people, planet impacts). The financial (profit) impacts are the life-cycle costs associated with the project (e.g., capital expenditures, operations and maintenance, replacement costs, residual value of assets). Life Cycle Cost Analysis [ADD ANCHOR LINK] can be used as the financial analysis in a TBL analysis. The social (people) impacts are the effects of a project on the broader community, quality of life or society. Finally, the environmental (planet) impacts are the effects of a project on the surrounding environment, habitat or climate. These three values presented together form the TBL valuation. The three separate accounts cannot easily be added up.

Triple Bottom Line Cost Benefit Analysis (TBL-CBA): also called screening level S-ROI, is a systematic evidence-based economic business case framework that uses best practice Life Cycle Cost Analysis and Cost Benefit Analysis (CBA) techniques to quantify and attribute monetary values to the Triple Bottom Line (TBL) impacts resulting from an investment. These TBL outcomes are typically represented as People, Planet, Profits or Social, Environmental and Financial. The framework quantifies these impacts in dollars over the life of the project and discounts them to the present in order to calculate the Net Present Value of an investment from the financial viewpoint of an organization, as well as from society’s perspective. An example of the financial benefits would be items such as cost savings on an energy or water bill; a social benefit could be the benefit of reduced flooding or improved health and safety; and an environmental benefit might be a reduction in CO2 emissions or enhanced water quality. The primary reason for adding the TBL qualifier to CBA is to make it absolutely clear that all relevant social and environmental factors must be rigorously quantified in dollars and included in the analysis. TBL-CBA differs from S-ROI in that the assessment uses readily available information for risks, opportunities, costs and benefits, whereas a full S-ROI uses input specific to the current project or policy. Further information on Wikipedia.

Type I Ecolabel: A Type I Ecolabel is a third-party program that assigns the label based on life cycle environmental preferability within a product category. The labeling scheme is voluntary, such as the Green Seal program. Type I Ecolabels are governed under the ISO 14024 standard.

Type II Ecolabel: A Type II Ecolabel is an informative self-declaration of claims. Type II Ecolabels are governed under ISO 14021.

Type III Ecolabel (also known as an Environmental Product Declaration or EPD): A Type III Ecolabel or Type III Environmental Product Declaration is a declaration of Life Cycle Assessment or Life Cycle Inventory data for a product or product family. It is intended to be used for comparison of products fulfilling the same function and is typically governed by ISO 14025. The LCA is currently implemented as a single-product LCA or footprint analysis and may be cradle-to-gate or cradle-to-grave. A product-specific Product Category Rule (PCR) provides guidance on modeling choices for the LCA and reporting requirements for the EPD.

W

Water consumption: quantifies the amount of water consumed in a process or activity, but does not show impact. Used for benchmarking only. Measured in cubic meters.

Water footprint: Analysis focusing on the life cycle water consumption of a product or service. It can either be represented by cumulative consumption in cubic meters or by water scarcity indices which take into account local water resources.

Weighting: the process of implementing values and preferences into an analysis, generally for aggregation of scores. Weights in LCA can follow different rationales, for example Individualist, Hierarchist and Egalitarian as applied in the weights assigned by ReCiPe. However, weights are entirely subjective and correspond to the preferences/priorities of the decision-makers. For the most part in LCA, weights take the form of “importance coefficients” -- unitless factors whose value is a representation of their importance (highest being most important). Importance coefficients are independent of the performance of the LCA. In LCA, is very common to use “equal weights” with each category being assigned the same value as a way to give all indicators the same level of importance. There are many ways to elicit weights: from expert panels to surveys. In the end, weighting is the process of applying such preferences to LCA in the aggregation to a single score.